Which Charles Pratt are you actually searching for?

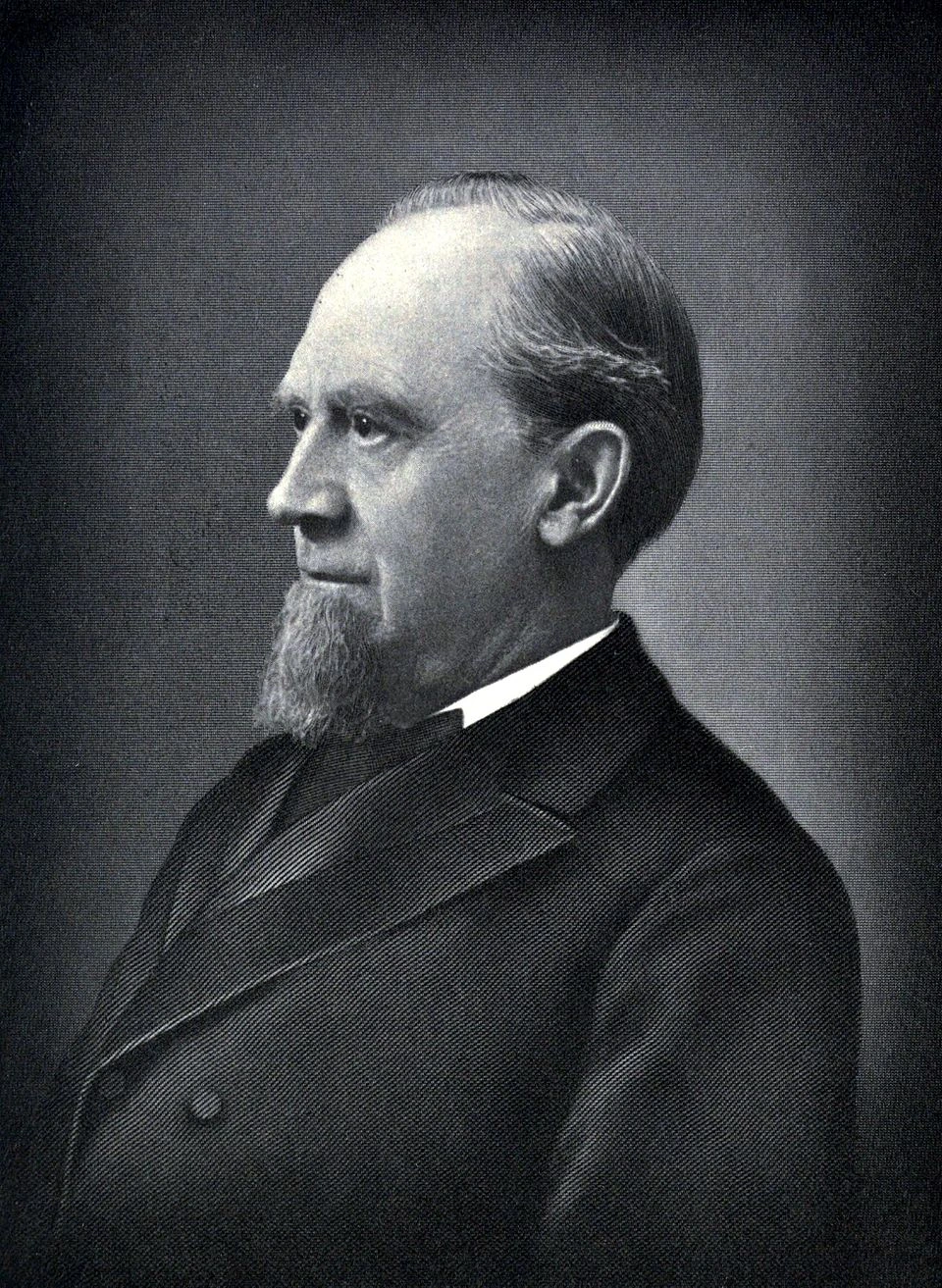

If you searched "Charles Pratt net worth," the most historically prominent person by that name is Charles Pratt (October 2, 1830 – May 4, 1891), the American oil-and-kerosene industrialist who built the Astral Oil Works refinery in Brooklyn, New York, recruited financier Henry H. Rogers, and founded Pratt Institute in 1887. He is widely regarded as one of the pioneering figures of the U.S. petroleum industry and was described by contemporaries as the richest man in Brooklyn during his prime. His son, Charles Millard Pratt (November 2, 1855 – November 27, 1935), carried on the family's oil and industrial business through Charles Pratt & Co., and his estate is actually the figure for which probate records survive. These two individuals are almost certainly the Charles Pratts that most net-worth researchers are looking for, and this article focuses on them specifically.

It is worth flagging upfront: there is no widely known living celebrity, athlete, or entrepreneur named Charles Pratt dominating search results as of April 15, 2026. If you are researching a different contemporary Charles Pratt (a lesser-known businessman, for example), the wealth-estimation methodology described below still applies, but the specific figures will differ. For comparison, readers interested in wealth profiles of other prominent Charles figures might find it useful to look at Charles Kuralt's net worth, which follows a similar research process grounded in career earnings and documented assets.

What net worth actually means and how estimates get built

Net worth is the value of everything a person owns (assets) minus everything they owe (liabilities). That is the baseline definition, and it sounds simple. In practice, calculating it for historical figures or private individuals is messier because most assets are not publicly priced on a daily basis. For a 19th-century industrialist like Charles Pratt, the primary assets were equity in Astral Oil Works, his Standard Oil stake after the merger, real estate including his Brooklyn home and the Glen Cove, Long Island country estate, plus philanthropic endowments and other investments. Liabilities would have included any outstanding business debts or obligations at the time of death.

Modern wealth trackers like the Bloomberg Billionaires Index and Forbes Real-Time Billionaires use a structured methodology: they pull public market data, filing disclosures, and reported information, then apply assumptions to value private holdings by benchmarking them against comparable public companies. Bloomberg converts all figures to U.S. dollars at current exchange rates and tracks changes daily as markets move. Forbes focuses heavily on top public holdings as of the last market close and notes that some illiquid assets (like primary residences) are often excluded from calculations. For historical figures like the Pratts, neither of those trackers applies directly; instead, the evidence base is probate records, estate filings, and contemporary accounts.

The data sources behind a Pratt wealth estimate

For Charles Pratt (1830–1891), no surviving probate valuation has been widely published in accessible form, but the wealth-source chain is well documented. He built Astral Oil Works in Brooklyn, which became one of the most successful kerosene refineries in the country. When Standard Oil (John D. Rockefeller's consolidating trust) absorbed Astral Oil, Pratt received Standard Oil stock in exchange, which meant his net worth became directly tied to one of the most valuable enterprises in American history. That transition from private refinery equity to publicly trackable Standard Oil shares is the single most important moment in understanding his fortune.

For Charles Millard Pratt (1855–1935), we have a more concrete data point: a June 1938 probate report filed with Kings County valued his estate at a gross value of $22,181,006, with a net estate value of $20,004,812 after a state tax of $3,305,062. That is the closest thing to a verified, sourced figure available for any member of the Pratt family, and it should be the anchor for any honest estimate of the family's generational wealth. Just as researchers studying figures like Charles Krasne's net worth rely on documented income streams and public filings rather than guesswork, the Pratt estate valuation gives a hard floor for the family fortune as of the late 1930s.

Primary source types researchers should use

- Probate and estate filings (county clerk records, estate tax returns): the Kings County 1938 filing for C. M. Pratt is the gold standard here

- Historical newspaper archives: Brooklyn Eagle, New York Times archives from the 1880s–1930s covered Pratt's business moves and philanthropy extensively

- Standard Oil historical records and trust dissolution documents (1911 Supreme Court antitrust ruling): these establish the value of oil trust stakes

- Pratt Institute financial records and founding endowment documents

- U.S. Census wealth schedules and tax records from the 19th century (where accessible)

The estimated net worth range and key assumptions

For Charles Pratt (1830–1891) at peak wealth (roughly the mid-1880s), a credible range in contemporary dollars is approximately $5 million to $15 million, which in inflation-adjusted 2025 terms translates to somewhere between $160 million and $500 million. That is a wide band, and intentionally so. The upper bound reflects the full value of his Standard Oil equity and real estate holdings if valued at market rates at time of death. The lower bound reflects a conservative reading that accounts for illiquid assets, potential encumbrances, and the fact that much of his wealth had already been transferred to the Pratt Institute endowment and family trusts before his death.

For Charles Millard Pratt (1855–1935), the hard number is cleaner: a net estate of approximately $20 million in 1938 dollars, which in 2025 purchasing-power terms represents roughly $430 million to $460 million. This figure is backed by an actual probate filing, making it the most defensible number in any honest Pratt net-worth discussion. The key assumption is that the 1938 valuation reflects all known assets at time of death with liabilities already netted out, which is what the filing structure confirms.

| Individual | Era | Estimated Net Worth (Contemporary) | Inflation-Adjusted (2025 USD) | Confidence Level | Primary Source |

|---|

| Charles Pratt (1830–1891) | Peak: mid-1880s | $5M – $15M | ~$160M – $500M | Moderate (no probate filing found) | Standard Oil records, historical accounts |

| Charles Millard Pratt (1855–1935) | Death: 1935 | ~$20M net estate | ~$430M – $460M | High (Kings County probate filing, 1938) | Estate filing, Kings County |

Breaking down where the Pratt wealth actually came from

Industrial and oil earnings

The foundation of the Pratt family fortune was kerosene. Charles Pratt built Astral Oil Works into a major refinery operation during the post-Civil War petroleum boom. Charles Pratt established and built the Astral Oil Works refinery in Brooklyn, New York blank" rel="noopener noreferrer">built Astral Oil Works. When Standard Oil absorbed Astral Oil, Pratt received equity in the trust, making him a significant stakeholder in the most powerful industrial corporation of the Gilded Age. Those oil dividends and trust distributions formed the primary income stream for both Charles Pratt and his son Charles Millard Pratt through the late 19th and early 20th centuries. Researchers familiar with how industrialist-era wealth compounds over generations will recognize this pattern, not unlike the kind of wealth trajectory you see documented in profiles of figures like Charles Cross's net worth, where a single career-defining move anchors everything that follows.

Real estate and property holdings

Charles Pratt owned significant Brooklyn real estate, including his well-documented Clinton Avenue residence, which was constructed after Astral Oil merged with Standard Oil. The family also maintained a country estate in Glen Cove, Long Island, and Charles Millard Pratt's sons each developed individual estates in the same area, suggesting substantial multi-generational real estate holdings. Real estate of this type (late 19th-century Brooklyn brownstone districts and Long Island estates) appreciated significantly over the 20th century, but for estate valuation purposes at time of death, the relevant figure is the appraised value at that moment, not subsequent appreciation.

Philanthropy and endowments (wealth deployed, not held)

Charles Pratt founded Pratt Institute in Brooklyn in 1887, endowing it with a substantial portion of his fortune. This is important for net-worth calculations because assets transferred to an endowment reduce personal net worth at time of transfer. Depending on when those transfers occurred relative to death, they may or may not appear in probate valuations. The founding endowment for Pratt Institute is therefore a subtraction from, not an addition to, any estimate of personal wealth at time of death.

Business ownership and investments

Beyond oil, the Pratt family's wealth was channeled into Charles Pratt & Co., the family business that Charles Millard Pratt joined at the start of his career. This company served as both a business entity and an investment vehicle, similar to how wealthy families of that era used holding structures to manage and grow industrial profits. The diversification from pure oil equity into broader investments is consistent with how the estate retained its multi-million-dollar value through the economic turbulence of the early 20th century.

How the Pratt fortune changed over time

The wealth trajectory of the Pratt family follows a recognizable arc: rapid accumulation during the petroleum boom of the 1860s–1880s, consolidation and diversification after the Standard Oil merger, generational distribution across multiple heirs and charitable institutions, and then gradual reduction through estate taxes and ongoing philanthropy. The 1911 antitrust dissolution of Standard Oil into 34 separate companies would have affected the value of any remaining Standard Oil equity held by the Pratt estate, though by that point Charles Pratt senior had been dead for 20 years. That AskHistorians discussion also addresses how Standard Oil was structured and how it was treated in terms of ownership and public trading versus private holding forms before and around the breakup The 1911 antitrust dissolution of Standard Oil into 34 separate companies.

Charles Millard Pratt's estate valuation in 1938 (with a gross of $22.18 million and net of $20 million) reflects the end state of this process: a fortune that had been partially distributed to family trusts, partially donated to philanthropic causes including Pratt Institute, and partially reduced by the Great Depression's impact on asset values during the 1930s. The $3.3 million state tax levied on the estate gives a concrete indication of how seriously state authorities valued the holdings, since estate tax assessments are based on independent appraisals rather than self-reporting.

For those tracking contemporary Charles figures across different industries, it is worth noting that the update cadence for historical wealth estimates is much slower than for living public figures like Charles Trippy, whose net worth shifts with platform revenues and brand deals, or Charles William Criss, where entertainment earnings and touring income change year to year. Historical estimates, once anchored by probate filings, tend to be stable unless new archival documents surface.

How to verify this estimate yourself

The most important thing you can do as a reader is separate the confirmed figure (the 1938 Kings County estate filing for C. M. Pratt) from the estimated figures (the inflation-adjusted range and the broader Charles Pratt senior valuation). The confirmed figure is verifiable through public probate records; the estimates require you to apply inflation conversion tools and make judgment calls about asset completeness.

- Search the Kings County (Brooklyn) Surrogate's Court records for the 1938 estate filing of Charles Millard Pratt. This is a public document and provides the gross estate, net estate, and tax figures.

- Use the Bureau of Labor Statistics CPI Inflation Calculator (available at bls.gov) to convert any dollar figure from 1935 or 1938 to 2025 dollars. A 1938 dollar is worth approximately $21–$23 in 2025 terms.

- Cross-reference the Standard Oil historical trust records (available through academic archives and the Rockefeller Archive Center) to understand the approximate value of Pratt's Standard Oil equity stake.

- Review Pratt Institute's founding documents and historical financial records to understand what portion of wealth was transferred to the endowment and when.

- Check historical Brooklyn Eagle newspaper archives (digitized through the Brooklyn Public Library) for contemporary reporting on Pratt's business dealings and estate.

- For any living or contemporary Charles Pratt you may be researching, apply the same framework: identify documented income streams, locate any public filings or disclosures, find comparable industry benchmarks, and build a range with clearly stated assumptions rather than a single unverified number.

One useful habit when researching historical wealth figures is to look for jewelry and luxury goods as a secondary indicator, since high-value personal property often appears in probate inventories separately from real estate and financial holdings. For example, researchers profiling figures like Charles Krypell routinely examine product lines and business valuations as part of a total picture, a similar methodology to checking probate schedules for personal property in historical estates.

The bottom line: for Charles Pratt (1830–1891), the honest answer is a range of $5 million to $15 million in contemporary dollars, inflation-adjusted to roughly $160 million to $500 million in today's money, based on Standard Oil equity and real estate holdings, with moderate confidence because no probate filing has been widely published. For Charles Millard Pratt (1855–1935), the documented net estate of $20,004,812 (1938) converts to approximately $430 million to $460 million in 2025 purchasing power, with high confidence because a verified probate filing exists. If you are searching for a different, contemporary Charles Pratt, apply the verification checklist above and build your estimate from documented sources outward, never from a single unverified number inward.